Remote hiring compliance involves labor law, taxes, contracts, intellectual property, and data privacy. The law depends on where the employee is, rather than where the company is located. Once a worker is in a different state or country, the company follows compliance requirements for that specific location.

Companies get into trouble with international remote staffing when they treat “contractor vs. employee” as a template decision rather than a country-by-country legal classification.

Most major jurisdictions use fact-based tests that can override what the contract label says. For example, calling someone a “contractor” doesn’t make them one if the relationship looks like employment.

This guide focuses on a compliant approach to international hiring taxes, a legally robust remote developer contract, and practical IP protection across borders. Moreover, we will explain the privacy/security layer (GDPR and CCPA) and how Employer of Record (EOR) and Professional Employer Organization (PEO) structures can reduce compliance exposure.

Contractor vs Employee Classification by Country

Whether you are hiring in the Americas, EMEA, or APAC, the name on the contract is secondary. What matters the most for compliance is the relationship between you and your employee/contractor. Modern labor inspectors now use automated data-matching between tax filings and social security contributions to flag hidden employment.

We broke down the specific criteria used by major jurisdictions to determine if your remote developer is truly an IT contractor or a misclassified employee.

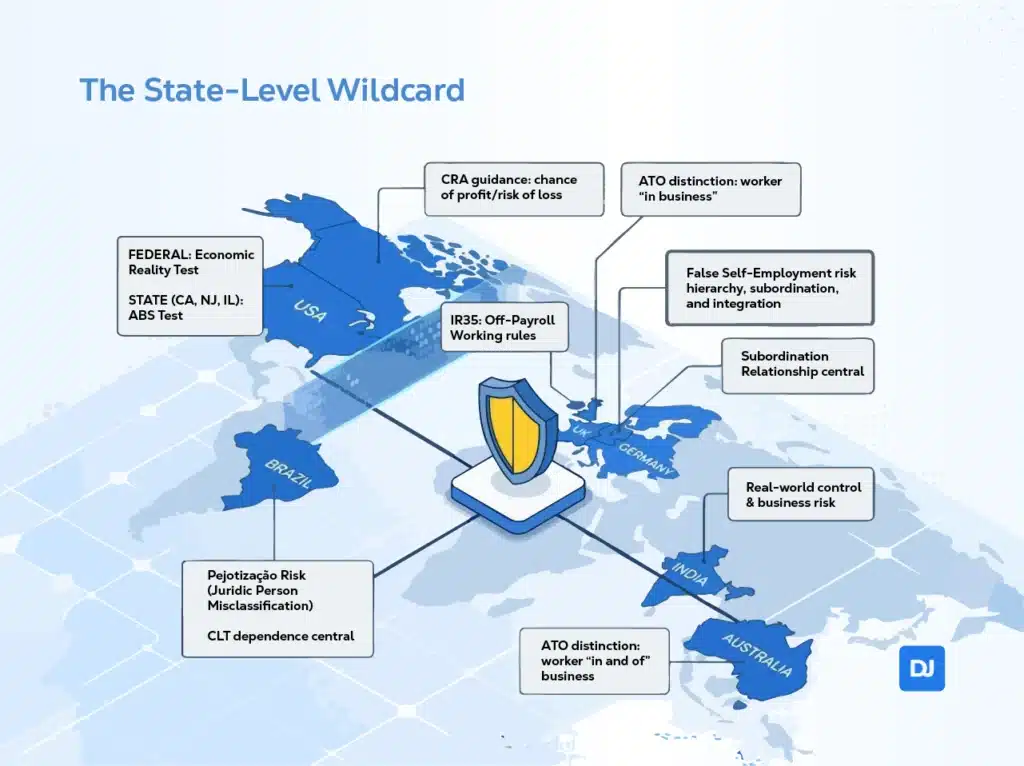

Remote Staffing Compliance in the United States: Contractor vs. Employee Rules

In the United States, federal and state authorities apply various tests to determine worker status. As of May 1, 2025, the U.S. Department of Labor (DOL) announced it relies on the “economic reality” framework outlined in Fact Sheet #13 (July 2008), as further informed by a reinstated 2019 Opinion Letter.

The 2008/2019 framework is generally considered more business-friendly, as it emphasizes the nature and degree of control, investment, and opportunity for profit/loss.

While the DOL will not enforce the 2024 rule from the Biden administration, it has not been formally rescinded. On February 26, 2026, the U.S. Department of Labor has just taken this a step further by officially moving to rescind the 2024 Rule entirely.

However, the 2024 rule remains in effect for private litigants, meaning workers can still sue employers under the tighter 2024 standard.

The Seven-Factor Framework (Current Enforcement)

While both standards use similar language, the DOL is currently focusing on these factors from Fact Sheet #13 (2008):

| Factor | Focus under Fact Sheet #13 (2008) | What They Look For |

| Control | Does the employer exercise substantial control over how the work is done? | Does the company set the schedule, or does the worker? |

| Profit/Loss | Does the worker have a real stake in the business’s success or failure? | Can the worker make more money by being efficient or hiring help? |

| Investment | Has the worker invested in their own facilities and equipment? | Does the worker provide “tools of the trade” (e.g., a truck vs. a laptop)? |

| Skill | Does the work require specialized skill and “business-like” initiative? | Does the job require specialized, independent expertise? |

| Permanence | Is the relationship intended to be permanent or indefinite? | Is it a 3-month project or an indefinite 40-hour-a-week gig? |

| Integration | Is the worker’s service an integral part of the business’s operations? | Is the worker performing a core function of the business? |

| Organization | Is the worker operating a truly independent business entity? | Does the worker have their own LLC, business cards, or website? |

The State-Level Wildcard

Regardless of what the federal DOL does, states like California, New Jersey, and Illinois often use the ABC Test, which is significantly stricter than even the 2024 federal rule. In those states, a worker is presumed to be an employee unless the business can prove all three of the following:

- A: The worker is free from control.

- B: The work is performed outside the usual course of the company’s business.

- C: The worker is customarily engaged in an independently established trade.

United Kingdom

In the United Kingdom, “off-payroll working” (IR35) rules ensure that workers who provide services through intermediaries (often personal service companies) pay broadly similar Income Tax and National Insurance as employees, when, but for the intermediary, the relationship would be treated as employment.

For many contractor-like arrangements, the key compliance question is whether the engagement is effectively “disguised employment,” because the tax treatment and payer responsibilities can change accordingly.

Canada

In Canada, the Canada Revenue Agency guidance emphasizes factors such as the worker’s chance of profit and risk of loss, plus other relationship indicators, in determining whether someone is self-employed or an employee.

A practical signal from CRA-style analysis is whether the person operates like an independent business. For example, does that person set pricing? Can they serve multiple clients? Do they incur expenses to earn income and bear genuine financial risk? The CRA explicitly discusses these factors.

Australia

In Australia, the Australian Taxation Office describes a core distinction: employees work in and are part of your business, while independent contractors provide services to a principal’s business.

This framing matters for remote staffing because “being part of the business” can show up in day-to-day reality: internal manager oversight, fixed schedules, mandatory stand-ups as if staff, use of company systems indistinguishable from employees, and long-term open-ended engagement.

Germany

In Germany, misclassification concerns revolve around concepts like “false self-employment”, hierarchy, subordination, and company integration. German social law reflects, frames, and repeatedly references these questions in compliance commentary.

The practical remote-work lesson: if a “freelancer” is treated like a team member (fixed hours, direct supervision, required attendance patterns, functional reporting lines, and limited independence), German-style risk increases even if the contract calls them a contractor.

France

In France, “subordination relationship” is central to distinguish employment from independent contracting. French legal analysis often centers on whether the client gives orders, monitors execution, and sanctions breaches. This approach echoes in summaries of French Supreme Court jurisprudence.

A common pitfall in remote developer arrangements is building a “contractor” relationship that includes employee-like sanctions (e.g., performance discipline through managerial authority) and tightly managed day-to-day methods rather than deliverable-based autonomy.

Brazil

In Brazil, the Consolidation of Labor Laws (CLT) defines an employee as a natural person providing non-occasional services to an employer, under the employer’s dependence, for a salary. That statutory formulation puts subordination (“dependence”) at the center of employment characterization.

For remote staffing in Brazil, the compliance issue is “pejotização”-style risk in practice. “Pejotização” comes from “Juridic Person”, in other words, a company. It happens when an employee utilizes a company while they are effectively managed as an employee under direction and ongoing integration.

Brazilian companies often ask employees to set up their own companies, so they are considered contractors and, therefore, not under the CLT jurisdiction. However, if the work is done under certain conditions, the worker is considered an employee the company owes the employee CLT’s rights.

India

In India, legal discussions frequently distinguish “contract of service” (employment) from “service contract” (independent contractor), and Indian jurisprudence has historically relied on tests including control and supervision, along with multi-factor analysis, as contexts evolved.

For a remote developer contract, you should assume India will also look at real-world control: who sets hours, who controls methods, whether the person is effectively part of the organization, and whether they bear business risk like an independent enterprise.

The Practical Framework For All Countries

Since country tests differ, the best global approach is to:

- Define the business need (project-based vs ongoing role)

- Select the engagement model (contractor, local employment, EOR), and

- Align daily operations, so reality matches the model.

Tax authority frameworks repeatedly stress that facts and the relationship reality control the outcome.

If you must use contractors cross-border, the strongest “universally helpful” operational pattern is deliverables and autonomy.

A contractor controls the means/methods, can work for others, and uses their own tools where feasible. Contractors also invoice per milestone, and are not embedded into HR processes (benefits, employee handbook rules, mandatory employee training), except for what is necessary for security and legal compliance.

IP Protection Across Borders

The protection of source code, patents, and trade secrets in a remote environment is fraught with jurisdictional challenges, as IP laws are territorial. Without well-drafted assignment clauses, a company might lose its IP for software developed by its international contractors.

The Conflict of Default Ownership

A critical nuance in global IP is that in many jurisdictions, ownership defaults to the human creator rather than the entity that commissioned the work. This is particularly true in civil law countries such as France, Brazil, and Germany, where the concept of “Moral Rights” is robust.

In India, Section 17 of the Copyright Act establishes the creator as the first owner of a work. While Proviso (c) allows for automatic ownership by an employer in a “contract of service” (traditional employment), no such automatic transfer exists for a “contract for service” (independent contracting). Consequently, software developed by an Indian contractor remains their property unless a written assignment is signed that identifies the work and specifies the rights transferred.

Moral Rights: The Civil Law Hurdle

Moral rights include the right to be identified as the author and the right to object to any “derogatory treatment” or modification of the work. In common law jurisdictions like the US and the UK, these rights can generally be waived in writing. However, in continental Europe (France, Germany) and Latin America (Brazil), moral rights are often “inalienable” and cannot be waived or transferred.

To mitigate this, companies should employ “licensing-type” provisions that grant the broadest possible rights to modify and exploit the work, ensuring the enterprise can iterate on its codebase without legal interference from the original developer.

In Brazil, any transfer of software rights must be registered with the Instituto Nacional da Propriedade Industrial (INPI) to be fully enforceable against third parties and to allow for tax-deductible royalty payments.

Best Practices for IP Assignment Clauses

Effective IP assignment in remote contracts requires more than a simple all rights reserved statement. Agreements must utilize “Present Assignment” language, stating the developer “hereby assigns” all rights rather than merely “agreeing to assign” them in the future.

Contracts should also include a “Further Assurances” clause, obligating the worker to assist in perfecting the title through local registrations or the signature of auxiliary documents, even after the termination of the engagement.

Moreover, here’s a summary of the nuanced understanding of international intellectual property law across the countries.

| Country | Default Ownership (Contractor) | Moral Rights Status | Registration Requirement |

| USA | Contractor (unless written) | Limited (mostly visual arts) | Voluntary (for litigation) |

| India | Contractor (unless written) | Strong (waivable) | Not mandatory for ownership |

| Brazil | Contractor | Inalienable | INPI Registration (for tax/3rd party) |

| France | Contractor | Inalienable | None |

International Hiring Taxes

International Hiring Taxes usually break into three layers: worker-level taxes, employer/payroll compliance, and corporate-level exposure (corporate residence and “permanent establishment” risk).

| Layer | Focus Areas |

| Layer 1: Worker-Level | Payroll tax/withholding for employees and cross-border payments/withholding for contractors. |

| Layer 2: Employer/Payroll | Local registration (direct or EOR), running compliant payroll, and social contributions. |

| Layer 3: Corporate-Level | Corporate Tax Residence (management and control) and Permanent Establishment (PE) risks. |

Payroll Tax and Withholding Obligations

When you hire someone as an employee, you take on payroll obligations where they work. For example, U.S. employers’ federal tax responsibilities include withholding and reporting rules explained in Internal Revenue Service Publication 15. It’s explicitly designed to describe employer responsibilities for withholding, depositing, reporting, and paying employment taxes.

In the UK, employers normally must operate PAYE (Pay As You Earn), the system used to collect Income Tax and National Insurance from employment. HMRC provides employer-facing guidance describing PAYE’s role in payroll.

The general remote-hiring compliance principle is: if the person is your employee in a country, assume you may need to:

- register as an employer locally (directly or via an EOR),

- run compliant payroll withholding, and

- handle employer social contributions and statutory reporting, even if the worker never visits your headquarters.

Cross-Border Contractor Payments and Withholding Documentation

Even with contractors, cross-border payments can trigger withholding and reporting obligations depending on the payer’s jurisdiction, the payee’s status, and the source of income.

For example, in the U.S., the IRS explains that foreign payees generally provide Form W‑8BEN (individuals) to a withholding agent/payer when the foreign person is the beneficial owner of amounts subject to withholding.

The IRS also notes that nonemployee compensation paid to nonresident aliens is reported on Form 1042‑S and that withholding may be required, reinforcing that “contractor” does not automatically mean “no tax compliance.”

Local Registration, Running Compliant Payroll, and Social Contributions

Managing payroll across borders requires more than just currency conversion. To stay compliant, companies must navigate the following three requirements:

1. Employer Registration

Most countries require you to have a local Tax ID and Social Security number before you can legally pay a worker. In the UK, this means registering for PAYE with HMRC; in Brazil, it requires registration with the eSocial system.

2. Social Security Contributions

Unlike the U.S., where the employer share of FICA Tax is roughly 7.65%, international rates can be significantly higher.

For example, French employers often face social charges upwards of 45%. And recently, the Social Security Ceiling (PASS) also increased by 2%, with the annual threshold now set at €48,060.

Meanwhile, Spanish employers may pay around 32% in contributions. Have in mind that the minimum wage in Spain is increasing constantly. And failing to budget for these can lead to a 20-30% surprise increase in the total cost of hire.

It’s worth noting that, in many EU jurisdictions, the “surprise” cost isn’t just the 30-45% social contribution. It’s also mandatory occupational medicine, insurance, and training taxes, which can add another 2-5% on top of the base social security rate.

3. Statutory Pay Cycles and Benefits

Compliance includes adhering to local norms such as the 13th-month salary (standard in Brazil and the Philippines), mandatory severance pay (often one month’s salary per year worked), and local holiday calendars that dictate when payroll must be processed to avoid late-payment penalties.

Corporate Residence and “Permanent Establishment” Risk

The difficult part of remote hiring is that a single person in the wrong role can create tax consequences that are out of proportion to their headcount. For example, signing contracts, acting like a local executive, or consistently working from a fixed home office in a way attributable to the company.

Two corporate-level risks matter most in remote staffing:

Corporate Tax Residence Risk

Some jurisdictions treat a company as a tax resident not only based on incorporation, but also based on where it is effectively managed. UK guidance in HMRC internal manuals summarizes that corporate residence analysis can hinge on where central management and control actually abides (with reference to established case-law framing).

For the U.S., OECD materials explaining residency for tax purposes emphasize that domestic corporations are treated as U.S. tax residents (even if also resident elsewhere), highlighting that “residence” rules are jurisdiction-specific and can create dual-residence scenarios managed by treaties.

Permanent Establishment (PE) / Taxable Presence Risk

Under the Organisation for Economic Co-operation and Development Model Tax Convention framework, PE analysis can consider whether a fixed place (including potentially a home office) constitutes a “place of business” of the enterprise and whether activities are sufficiently permanent and attributable to the business (with additional nuance for preparatory/auxiliary activities).

The OECD 2025 Update: New Benchmarks for Remote Work

On November 19, 2025, the OECD released a pivotal update to the Model Tax Convention, introducing a modernized framework for assessing PE risks in the context of cross-border remote work. This update moves away from rigid 2012 guidance toward a “facts-and-circumstances” analysis characterized by two primary components.

The Temporal Test (50% Limit)

A remote location is generally not considered a “fixed place of business” if an employee spends less than 50% of their total working time in that jurisdiction over any 12 months. This serves as a “safe harbor” for incidental remote stints or digital nomad lifestyles.

The Commercial Reason Test

For arrangements exceeding the 50% threshold, authorities examine whether the employee’s physical presence serves a genuine business purpose for the company, such as serving local clients or accessing regional markets. If the location is chosen solely for employee convenience or retention, the risk of a PE is mitigated, though not eliminated.

Agency and Service-Based Tax Nexus

Beyond the physical presence of an employee, companies must monitor “Agency PE” risks. This occurs when a “dependent agent” (often a remote sales representative or executive) habitually exercises decision-making power to conclude contracts in a foreign country.

Similarly, a “Service PE” can be triggered if an enterprise provides ongoing services in a country for a duration that exceeds specific treaty-defined periods, even in the absence of a fixed office.

Mitigation of Global Tax Liability

To safeguard against surprise tax liabilities, companies should implement a centralized workflow for international remote work requests. This includes tracking where every employee is working using geo-fencing or travel trackers, setting clear thresholds for “work-from-abroad” days, and restricting high-risk roles (such as senior leadership and sales) from operating in jurisdictions where the company lacks a registered entity.

The following table summarizes the primary categories of Permanent Establishment risk:

| PE Type | Triggering Mechanism | Common Remote Scenario | Risk Level |

| Fixed Place | Ongoing presence in a location | Employee home office > 50% time | Moderate |

| Agency PE | Dependent agent signing contracts | Remote sales rep concluding deals | High |

| Service PE | Long-term service delivery | Dev team on a 6-month project abroad | Moderate |

| Management PE | Effective place of management | Executive working from a second home | Critical |

How to Manage International Hiring Taxes in Practice

A workable governance model is to treat taxes as a role design problem, not only a payroll problem.

Assess fiscal/PE presence early if the remote worker has executive or commercial authority. Don’t wait for the contract to be signed or the workload to be officially announced to conduct this analysis. OECD and national guidance consistently point to authority, permanence, and business attribution as the critical facts.

For pure engineering roles, PE risk can be lower. However, it can still arise if the home office becomes at the company’s disposal or if a founder/key executive works abroad as a habitual base. Therefore, location tracking and role boundaries remain important.

Data Privacy and Cybersecurity

For companies hiring in the United States and the European Union, the compliance requirements for 2026 are increasingly centered on automated systems and proactive security audits.

| Feature | California (CCPA/CPRA) | European Union (GDPR/AI Act) |

| AI Regulation | Focus on ADMT (Automated Decision-Making Technology) | Governed by the EU AI Act (Hiring is “High Risk”) |

| Audit Focus | Cybersecurity and Risk Assessments | Data Protection Impact Assessments (DPIA) |

| Sensitive Data | Includes Neural Data and Biometrics | “Special Category” includes Trade Union/Health |

| Enforcement | California Privacy Protection Agency (CPPA) | National Data Protection Authorities (DPAs) |

CCPA and CPRA: The California Mandate

As of January 1, 2026, the California Privacy Protection Agency (CPPA) has finalized a series of regulations that significantly expand the scope of the CCPA. These updates introduce three major compliance requirements for covered businesses:

Annual Cybersecurity Audits: Mandatory for organizations processing the data of 250,000 or more residents or sensitive info of 50,000 or more consumers. These audits must be performed by independent, qualified auditors and assessed against standards like NIST or AICPA.

Privacy Risk Assessments: Required for high-risk data processing, including the use of “Automated Decision-Making Technology” (ADMT) for employment decisions like hiring, promotions, or compensation.

ADMT Disclosures: Businesses using AI or algorithms for significant decisions must provide a “Pre-Use Notice,” explain the logic of the system, and grant employees the right to opt out of automated processing (a significant operational hurdle for HR departments).

GDPR and the Trans-Atlantic Nexus

The GDPR remains the most comprehensive privacy framework, applying to any entity processing the data of EU citizens, regardless of the employer’s location. HR data (including health details, union memberships, and biometric data) is classified as “special category data” and requires a valid lawful basis for processing beyond simple consent.

For US-based firms hiring in the EU, cross-border data transfers must be secured using Standard Contractual Clauses (SCCs) to ensure that employee data enjoys the same level of protection once it leaves the EEA.

Operational Security for Remote Staffing

Beyond legal filings, organizations must implement technical safeguards to prevent data exfiltration. This includes providing company-supplied hardware, utilizing Virtual Desktop Infrastructure (VDI), and disabling functionality like USB ports or print-screen on development machines.

The 2026 CCPA update also expands the definition of “sensitive personal information” to include neural data, reflecting the emergence of brain-computer interfaces and advanced biometric monitoring in the workplace.

Contract Essentials

The remote staffing arrangement is governed by a triangular agreement between the client company, the EOR (or service provider), and the individual worker.

While it is a three-way relationship, there are usually two separate contracts:

- The Service Agreement (Client with the EOR).

- The Employment Contract (EOR with the Worker).

The Client and Worker often have no direct legal contract, which is how the Client avoids “Permanent Establishment” risk.

Essential EOR Service Agreement Clauses

A robust EOR contract must clearly delineate the division of labor. The EOR provider should handle payroll, tax withholdings, and legal compliance, while the client company manages day-to-day tasks and performance. Key clauses include:

- Tax Indemnification: A crucial provision where the EOR assumes financial responsibility for penalties or interest resulting from errors in local statutory filings. This is the “gold standard” for a contract.

- Be aware that many EORs try to limit their liability to a multiple of their service fee.

- Multiplier of Fees: EORs often limit their total liability to a specific multiple of the service fees paid by the client, for example, 3x the fees.

- Time-Based Cap: Liability may be capped at the fees paid in the last 12 months.

- Fixed Monetary Amount: Some contracts cap liability at a fixed dollar amount, regardless of the actual damages incurred.

- Exclusion of Consequential Damages: Many EOR contracts exclude liability for indirect, consequential, or punitive damages.

- Be aware that many EORs try to limit their liability to a multiple of their service fee.

- Termination and Migration: The agreement must outline a clear exit plan, detailing how employees can be migrated to another provider or the client’s own entity if the partnership ends.

- Data Protection Agreement (DPA): A mandatory document specifying how employee data will be handled in accordance with GDPR or CCPA requirements.

Localized Employment Contracts

Don’t use a master contract template across multiple countries. Employment standards are set at the local level, including notice periods, overtime thresholds, and mandatory holidays.

For instance, UK employees are entitled to at least 28 days of paid leave, and Indian employees may have a statutory right to specific maternity and gratuity benefits that cannot be waived by contract.

US companies often mistakenly try to include at-will termination clauses in European or Latin American contracts. In most of the world, at-will employment does not exist, and attempting to include it can make the contract void or lead to heavy fines.

How EOR Solves Compliance

An Employer of Record (EOR) is a third-party organization that legally employs the worker in another country, while you have full control of the employee. In short, EOR serves as the infrastructure of your company’s growth, allowing for the issuance of compliant offer letters and localized payroll.

EOR Services handles all legal and compliance issues associated with working internationally. It takes a process that would require months of waiting and tens of thousands of dollars, and turns it into something that takes a day to accomplish.

What EOR Does Not Automatically Solve

An EOR can significantly reduce employment-law compliance friction (local payroll, statutory benefits, compliant employment agreements), but it does not automatically eliminate:

1. Permanent Establishment Risk

If your business activities in-country meet PE thresholds (e.g., dependent agent authority to conclude contracts), since PE analysis attaches to the enterprise’s activity footprint, not only payroll mechanics.

2. Data Protection Obligations

GDPR/CCPA duties apply based on personal data processing roles and transfers. Therefore, you still need appropriate contracts, SCCs where relevant, and security controls.

3. IP Ownership Discipline

You still must ensure invention/IP assignment and enforceable clauses, especially if any contractors are used alongside EOR employees.

Conclusion

Dealing with remote hiring compliance requires a jurisdiction-first approach. With an Employer of Record (EOR), companies can offload the heavy lifting of localized payroll and statutory benefits.

However, the ultimate responsibility for Permanent Establishment (PE) risk and the integrity of IP assignment remains with the company.

That said, building a compliant remote team doesn’t have to be a legal minefield. We help high-growth companies bridge the gap between global talent and local regulations with:

- Localized Contract Audits: Ensure your IP and termination clauses are enforceable in 150+ countries.

- EOR Transition Strategies: Seamlessly move from risky “contractor” models to fully compliant employment.

- 2026 Privacy Frameworks: Implement the technical and legal safeguards needed for CCPA and GDPR compliance.

We fully support your legal compliance, so you can focus on what really matters: your business.

Contact our Compliance Experts Today!